Examples of filling out the book of income and expenses for SP. Key points and features of filling in the book of income and expenses for the object "income minus expenses"

An indispensable register of tax accounting is the book of income and expenses for individual entrepreneurs. Entrepreneurs must keep a journal on the Unified Agricultural Tax and the simplified tax system, for UTII and OSNO it is not required, the obligation is provided for by the Tax Code, Art. 346.24. Data accounting forms the basis for calculating income tax and preparing a tax return. The book should be filled out with special care in accordance with the requirements of the tax authorities. If violations are found, the individual will be fined.

How to maintain and fill out a book of income and expenses for individual entrepreneurs on the simplified tax system in 2019: a sample

KUDiR start after the adoption of simplified income tax. Each calendar year a new register is opened. The book can be completed electronically or on paper. At any time of the tax year, it is allowed to change the form of maintaining KUDiR.

After 2013, the book of income and expenses for individual entrepreneurs is not subject to certification by the Federal Tax Service. If there was no commercial activity, a "zero" form should be issued.

Before filling out the paper version, you must number the pages and carefully stitch the book. On the last page, the number of sheets is prescribed and stamped with a signature.

The e-book is completely printed out after the end of each quarter: each form of all sections is displayed. After the end of the year, it is drawn up similarly to the paper version.

The paper version is filled with dark ink. In the records it is better to take into account rubles and kopecks. The use of corrective agents is strictly prohibited. Any corrections must be made by crossing out with a horizontal line and then writing the correct value at the bottom or top of the line. Corrections in the printed e-book are made in the same way.

A sample of filling out the book of accounting for income and expenses (KUDiR) for individual entrepreneurs on the simplified tax system 6% in 2019 is located at.

KUDiR for individual entrepreneurs on the simplified tax system 6%

The book contains data important for the calculation of income tax. The USN 6% declaration must contain information from the register. For simplifications, "income-expenditure" books are adapted. Forms with rules of conduct were introduced in 2013 and continue to be valid today.

The structure of KUDiR IP on the simplified tax system 6% and filling rules

The register contains a title page and four sections. The book of accounting for income and expenses for individual entrepreneurs on the simplified tax system 6% is kept in two sections of "revenues":

Basic rules for entering information:

- Enter data on business transactions that are taken into account when calculating income tax;

- A primary document is attached to each entry;

- The chronology of operations is observed. New data is entered in separate lines. There is no layout on any basis;

- All entries are made in Russian letters.

The simplified taxation regime allows you to register in the book of basic data on profit from the sale of products and non-operating income. However, not all receipts will be taken into account for calculating payments to the Federal Tax Service. The book of income and expenses of an individual entrepreneur on simplified taxation does not contain income for which a single tax is not calculated. If they are entered in a book, they must be displayed in a special way.

"Simplified" tax does not apply to:

- Profits from the patent system and imputation;

- Dividends, prizes and other income listed in Art. 346.15 paragraph 3.

Income is not:

- Advances returned to buyers;

- Money transferred by mistake, and then returned to counterparties;

- Money for the return of marriage;

- Erroneous credits;

- FSS compensation for sick leave;

- Deposits for bidding;

- Refunded taxes;

- Competitors' assignments.

The journal of income and expenses of an individual entrepreneur on a simplified basis may contain expenses:

- Spending government subsidies to support small businesses or help self-employment for the unemployed;

- Payments under Art. 346.21 of the tax code of paragraph 3.1.

With the simplified tax system of 6%, the tax will be reduced due to:

- Payments for compulsory insurance (social, medical, pension).

- Contributions for VHI, if the insurance is not more than a three-day benefit.

- Three-day sick leave not covered by VHI.

- The amount of the trading fee, if the individual entrepreneur is its payer.

When taking into account the above, the tax can be reduced by 50%.

Filling order

The book of income and expenses of an individual entrepreneur is filled out in a certain sequence, taking into account the nuances for the simplified tax system 6%.

Title page

It is allowed to fill out the title page arbitrarily, adhering to a number of recommendations:

- The OKUD code is not provided for by the State Standard for KUDiR;

- "Date" - the day of the first entry in the log;

- OKPO for individual entrepreneurs do not fill out;

- The address must match the prescribed data in the constituent documents;

- Indicate each account number with the name of the bank in which it is opened.

You can download the book of accounting for income and expenses for individual entrepreneurs on income tax at the link.

Section 1

The first section consists of tables for each quarter and a certificate, which is not required under the simplified tax payment system.

The first section consists of tables for each quarter and a certificate, which is not required under the simplified tax payment system.

Important features:

- The numbering of the first column is end-to-end for the entire reporting period;

- In the second column, it is better to additionally indicate the name of the primary document;

- Income must be paid on the day the money is received. State subsidies are written in the amount of expenses incurred at the expense of subsidies. Do not make contributions that are not related to income. If there is a refund to the buyer, then its amount is recorded in the fourth column with a “-” sign on the day of transfer;

- The fifth column should indicate the funds spent from the state subsidy, documented.

Section 4

The fourth section reflects expenses that reduce the amount of tax. Important:

- Continuous numbering in the first column;

- In the second column, the number, date and name of the document;

- In the third column - the month for which contributions were paid;

- Columns 4-9 should contain the amount of expenses. The individual entrepreneur fills in columns 4 and 6 with the amount of contributions for employees and himself;

- Column 10 is summing up by rows.

KUDiR for individual entrepreneurs on the simplified tax system 15%

The book of income and expenses for individual entrepreneurs on the simplified simplified tax system 15% has additional sections that are important for the tax authorities. It is a separate register.

The businessman additionally fills in the "Section 1 Help". It indicates the total profit and expenses for the tax period. The difference between last year's tax and its minimum size is important. The taxpayer has the right to take into account this difference in the current period.

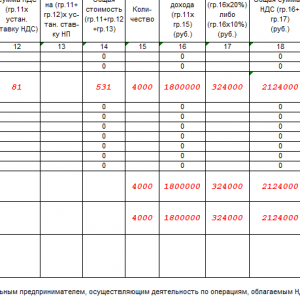

Organizations on the simplified tax system 15% must fill out Section 2. It is divided into quarters. They include fixed assets and intangible assets with a cost. Columns 7-8 must be filled in by individual entrepreneurs who have switched to a grace period after accounting for intangible assets with fixed assets. In column 10, enter the share of the cost taken into account in the income period (for new objects it is 100%).

You can study the sample filling in KUDiR for IP on the simplified tax system 15% Section II in Excel format at.

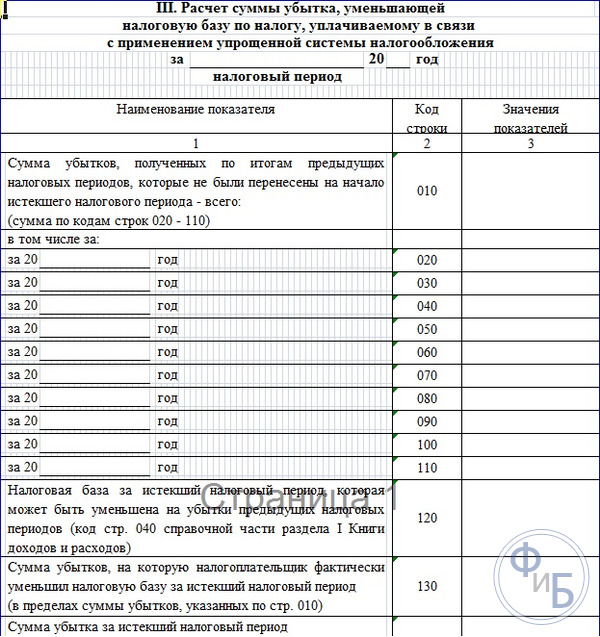

Section III "Calculation of the amount of losses". It includes losses for the previous calendar year. They are written line by line with subsequent decoding. In line 120, the tax base is inserted from the first section (Article 040). The next line writes the amount of losses to reduce income tax this year. Starting from line 160, they make losses to the organization, which will be taken into account in the next period.

An example of filling out the third section in Excel format is located at.

KUDiR for IP on UTII

Downloading a free book of income and expenses for individual entrepreneurs on UTII in 2019 in any format (pdf, xls, doc) does not make sense. This taxation regime does not provide for the mandatory presence of KUDiR. An individual entrepreneur can keep records of profits in a simple journal - UTII is a fixed taxation regime. The tax is not calculated from real income: the calculation takes into account a physical indicator with a correction factor.

Responsibility for violations in the conduct of KUDiR

Keeping a book of income and expenses of IP is mandatory. Its absence is a gross violation of accounting for commercial activities. Article 120 provides for punishment in the form of a fine, the amount of which determines the seriousness of the violation. The minimum amount is 10 thousand rubles.

According to Article 23 of the Tax Code, the book must be kept for 4 years after the end of the tax period.

An entrepreneur must take a responsible approach to accounting for economic activities. KUDiR is the connecting link of IP documentation. With its help, it is easy to structure work, organize documents and eliminate problems with the Federal Tax Service. Most keep a book for tax inspections, but it will become an important assistant in accounting.

Video: about KUDiR for IP

The obligation of an individual entrepreneur to conduct KUDiR is enshrined in Art. 346.24 of the Tax Code of the Russian Federation. Therefore, the individual entrepreneur is not entitled to refuse to maintain tax records according to the specified form. Moreover, the absence of KUDiR may threaten the entrepreneur with a fine of 10,000 rubles, and if the book has not been kept for two or more years - 30,000 rubles (Article 120 of the Tax Code of the Russian Federation).

How is KUDiR conducted

It is necessary to open a new KUDiR for each calendar year. At the same time, the individual entrepreneur himself decides how to keep the book - on paper or in electronic form. Having chosen the electronic version of KUDiR, the individual entrepreneur must print the book at the end of each reporting period and at the end of the year.

A book that is initially kept on paper or that is printed at the end of a calendar year must be laced and numbered. On the last page of the KUDiR, it is necessary to indicate the total number of pages contained in it and certify it with the signature of the entrepreneur and his seal, if any.

In KUDiR, an entrepreneur reflects business transactions that affect the amount of tax in chronological order based on primary documents.

How to fix errors in KUDiR

If an individual entrepreneur made a mistake in a laced and numbered book, then the entrepreneur can correct it like this:

- cross out the erroneous entry;

- make the correct entry, indicating "Corrected believe";

- indicate the date of correction;

- indicate your last name, initials and sign;

- certify the correction with a seal (if any).

What sections of KUDiR fill IP

The composition of the KUDiR depends on the object of taxation chosen by the entrepreneur. If he chose the object "income", then he fills in:

- section I "Income and expenses";

- section IV. In it, he will be able to reflect the amounts of contributions to extra-budgetary funds and some other expenses for which he can reduce the calculated tax (clause 3.1 of article 346.21 of the Tax Code of the Russian Federation).

Those entrepreneurs who have chosen “income minus expenses” as the object of taxation will fill in.

The book of income accounting for individual entrepreneurs on the simplified tax system is a mandatory type of reporting for an individual entrepreneur and it is through it that his activities are monitored. It has a standardized form approved by the Ministry of Finance of the Russian Federation. The rules for filling it out are strictly regulated by Russian law. In this book, business transactions are kept, and then taxes are calculated based on its data. Therefore, the tax inspectorate tries to control the correct filling of the accounting book.

Today we will consider how this book of accounting for individual entrepreneurs applying the simplified tax system from “Income” in 2017 should be filled out. We will tell you what to consider when filling out forms, not to pay special attention. The article will provide examples of filling out book forms. Filling out the book yourself, subject to our recommendations, is not difficult at all, today we will tell you in detail how to do it.

Separately, in our article we will consider the innovations of 2017. We will tell you in detail what has already changed in 2017 and what else they plan to change in the very near future.

Rules for maintaining a book of accounting for income and expenses

KUDIR- a book of accounting for business operations, which is mandatory maintained by individual entrepreneurs working on the simplified tax system.

Consider keeping a ledger of individual entrepreneurs working for the ONS with taxation of income at a 6% tax rate.

All individual entrepreneurs applying the simplified tax system for taxation must conduct their own KUDIR.

KUDIR- this is a type of IP reporting and it must be filled out regularly. Note that the tax inspector has the right to demand it and the entrepreneur is obliged to provide his KUDIR at the first request. In case of failure to provide correctly completed reports, a fine may be imposed, as well as for any other reports not submitted in a timely manner.

If, at the first request of the tax inspector, the entrepreneur could not provide KUDIR, he may be fined 200 rubles (see Article 126 of the Tax Code). If the accounting book is not found during the on-site inspection, the fine may already be - 10,000 rubles (see Article 120 of the Tax Code). If the individual entrepreneur was unable to provide accounting books for more than one year, then there is already a fine of 30 thousand rubles. If the tax authorities can prove that the lack of accounting for entrepreneurial activity has led to an underestimation of taxes, then the individual entrepreneur faces a fine of at least 40 thousand rubles.

However, we note that the requirement to present KUDIR must be executed in writing by an employee of the Federal Tax Service and can be presented during an on-site tax audit or in a number of other cases.

KUDIR refers to tax registers, which are the basis for the calculation of taxes, and therefore, its absence is tantamount to a violation of the rules for keeping records of income and expenses.

Now, as before, it is not required to submit KUDIR for regular checks at the Federal Tax Service Inspectorate.

Its form is the same for all individual entrepreneurs, but for different tax regimes, the methods of maintaining it are somewhat different.

KUDIR can be kept in the old way - on paper, making notes by hand, you can keep an electronic version on a computer and, if necessary, print it out. Now there are online services for maintaining KUDIR.

You can choose any of the accounting options, the main thing is to keep it correctly and be able to print, number, sew and present to the tax authorities at the right time.

KUDIR has an annual reporting form, i.e. For every new year, a new book is launched. At the same time, the book for the past reporting period is printed, numbered, stapled, certified by the seal of the individual entrepreneur (if any) and his signature. This book is subject to mandatory storage and the tax authority has the right to conduct an audit for the last three years.

If in the past year the individual entrepreneur did not conduct commercial activities, then a “zero” book should be printed and stitched together. If there were unfilled sections of the book, then they are also numbered and filed.

KUDIR is an annual IP reporting form. It is worth remembering this and understanding that the same requirements apply to it as to any other reporting. It is standardized and has a shelf life of 4 years.

If an individual entrepreneur has small annual turnover, then the ledger can be kept on paper, making notes by hand.

If the turnover is large, then it is better to keep records using specialized services. Perhaps, and just keep on the computer in excel.

In the accounting book, each operation is recorded in chronological order on a separate line, and it must be documented. The supporting documents are usually: invoices, payment orders, checks, contracts, etc.

The main general rules for maintaining KUDIR for individual entrepreneurs on the simplified tax system for "Income":

- KUDIR is an annual reporting form and therefore every year an entrepreneur must start a new accounting book, for a new calendar year - a new tax period

- entries in the book should be made line by line, i.e. one line - one operation

- records are kept in chronological order

- records are kept only in full rubles

- at the end of the reporting tax period, in this case, the calendar year, KUDIR should be printed

- unfilled sections of the book are still printed

- if the individual entrepreneur did not conduct any commercial activity during this year, he prints out a "zero book"

- at the end of the annual tax period, the accounting book is numbered and stapled, certified by the signature of the individual entrepreneur, if there is a seal, it is also certified by the seal

- the ledger must be kept for 4 years

- replenishment of the current account is not income from entrepreneurial activity, and such transactions are not recorded in the ledger

- the KUDIR form is a unified reporting form, its forms were approved by order of the Ministry of Finance No. 135n on 10/22/2012.

The standardized form of KUDIR contains:

- The title page on which the data of the IP taxpayer is registered

- Section 1 "Income and expenses", it is filled in by all individual entrepreneurs

- Section 2 "Expenses on fixed assets and intangible assets" - IP on the simplified system "Income" is not filled out

- Section 3 Calculation of the amount of loss - IP on the simplified tax system "Income" is not filled out

- Section 4 Insurance premiums - filled in by all individual entrepreneurs.

We have outlined the basic rules for maintaining KUDIR and the requirements for it. Next, we will analyze all sections of the accounting book in more detail and the rules for filling it out.

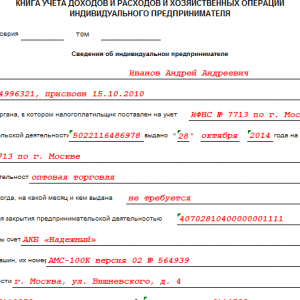

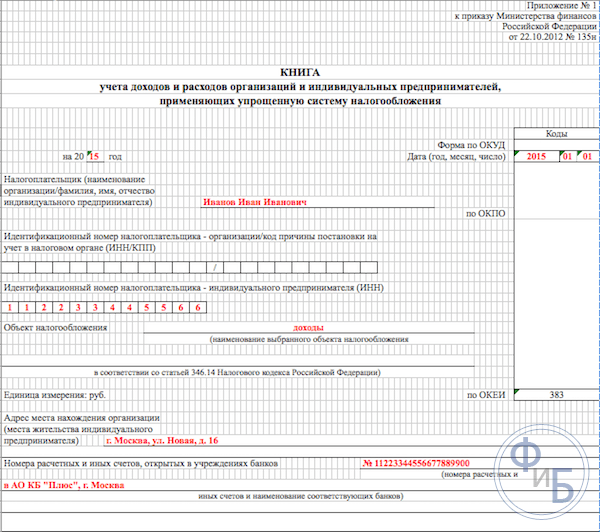

Filling out the accounting book begins with the design of the title page:

- the column "Form according to OKUD" is not filled out

- in the column "Date" the date of opening of the book is entered - the date of its first recording

- fill in the field for which period the book is open - for 2017

- the OKPO field indicates the code from the statistics

- in the column "Taxpayer" enter the full name of the individual entrepreneur

- in the TIN / KPP column, indicate the corresponding IP numbers

- in the column "Object of taxation" - write "Income"

- in the address bar indicate - the address of the IP

- further at the bottom of the page, fill in the fields of bank details - indicate the details of the IP settlement account.

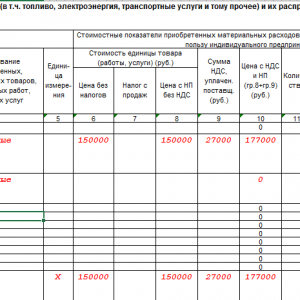

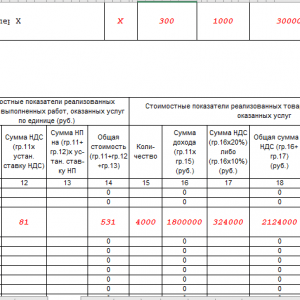

In section 1 of the ledger, individual entrepreneurs who are in the income tax regime record their income. The form is designed for quarterly completion, it contains 4 tables. Each operation is written on a separate line, you can add the number of lines, if necessary. The tables have five vertical columns that need to be filled in, as follows:

- numbers of operations p / p, operations are in chronological order

- date and number of the transaction basis document, the dates of invoices, payments, etc. are indicated here.

- the content of the operation - it is necessary to briefly reflect its essence

- in the income column - write down the amount of income received

- column expenses - for individual entrepreneurs with taxation of only income, is not filled out.

And so, section 1 is filled in sequentially throughout the year.

We only note that, for example, cash receipts are summarized per day and reflected in one entry, the basis of the operation is the Z-report. Thus, we enter the date and number of this cash report in the table. You can do the same with other similar incomes. Upon receipt of the flow of payments to the current account, you can focus on the daily bank statement.

Note that sometimes there are cases when you need to make a payment refund, then an entry is made in the income column in the book, as usual, but with a minus.

After the end of each quarter, the section sums up the total numerical results in the corresponding rows of the tables. In specially designated lines, summed accruing results for six and nine months are reflected, the annual total is calculated.

In the expenditure column, entries for this taxation system are made extremely rarely, for example, if expenditures were made on funds received under the SME support program from state subsidies. These amounts must be reported in both income and expense columns so that they do not contribute to the taxable base.

Note that there are other non-taxable incomes, they do not need to be recorded in KUDIR. Often, individual entrepreneurs receive income from sales and income "out of sales", these concepts must be separated.

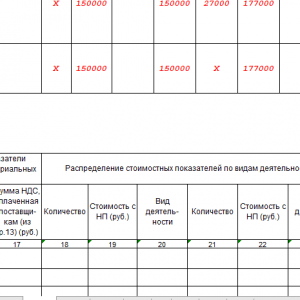

Completion of Section 2 "Calculation of expenses for the acquisition of fixed assets and intangible assets"

Completion of Section 3 "Calculation of the amount of loss reducing the tax base"

This section, IP on the simplified tax system only for income, is not filled out. It is intended for individual entrepreneurs who also keep track of expenses. Therefore, in the printout of the accounting book for the reporting period, this section will be filed blank.

Completion of Section 4 "Expenses that reduce the amount of tax"

In section 4, the amounts of contributions paid quarterly must be recorded and in the corresponding lines data are given in cumulative totals for six and nine months, the annual total is calculated. The columns of the table contain each of the insurance premiums that must be specified. Contributions are also indicated for employees if they were hired by an individual entrepreneur during this period. Further, advance tax payments must be taken into account when calculating the taxable base within the established limits.

If the individual entrepreneur has employees, then the following payments must be indicated in the section:

- contributions made from employees' salaries

- sick leave payments paid from the individual entrepreneur's own funds

- voluntary insurance payments

- fixed amounts of insurance premiums that were paid by the individual entrepreneur for himself

In 2016, the following innovations appeared for individual entrepreneurs on the simplified tax system under the taxation system from “income”:

- The procedure for filling out section 4 was clarified, regarding the entry in a fixed amount of insurance premiums.

- KUDIR was supplemented with a new section 5 "Amounts of the sales tax", which will reflect the amount of the paid sales tax.

- A new legislative rule has appeared that income received by an individual entrepreneur from foreign organizations controlled by him is not recorded in the KUDIR section 1 column 4. Taxation of such income is carried out separately.

Now let's talk about this in more detail.

It should be noted here that since 2017 Art. 430 of the Tax Code on fixed insurance premiums. That is, at the legislative level, there was a combination of insurance premiums for the minimum wage and contributions of 1% from incomes of more than 300 thousand rubles. These new rules apply to individual entrepreneurs who work without the involvement of employees, and who are on the simplified tax system from “income” and pay only their insurance premiums.

This means that now these individual entrepreneurs in the ledger will record all their deductions for compulsory insurance: both from the minimum wage and 1% from incomes of more than 300 thousand rubles in a fixed amount. Previously, until 2017, tax inspectors often refused to reduce the amount of 6% tax due to "1% contributions". Accordingly, questions often arose when filling out KUDIR.

The emerging norm of legislation on controlled foreign organizations is designed to clearly distinguish at the legislative level the taxation systems for individual entrepreneurs when paying a single tax on a simplified system and the application of income tax rates. Thus, now the tax code (see article 248) clearly states that income from foreign IP companies does not fall under the simplified tax system. Income tax must be paid on such income.

At the end of 2016, the KUDIR form was finalized - a new fifth section was included in it. However, the new form of the book will begin to be applied only from 2018, and accounting in the coming 2017 will continue to be kept according to the books of accounting of the previous sample.

A new section of the book deals with accounting for sales tax, which will reduce the amount of single tax paid. Note that the sales tax is still valid only in Moscow. The new section will be filled in similarly to other sections of the book, i.e. in chronological order, indicating the details of the documents - the grounds for business transactions.

Conclusion

The book of accounting is the main form of reporting for an individual entrepreneur, it reflects operations for the implementation of its commercial activities. The form of the book is standardized, the rules for filling it out are prescribed by law. When conducting it, all applicable legal provisions must be observed.

The Tax Inspectorate supervises the payment of taxes from the commercial activities of entrepreneurs, namely through control over the keeping of records of commercial transactions. For non-compliance with the rules for maintaining KUDIR, the law provides for the imposition of fines on entrepreneurs.

The article examined in detail the filling in of sections of the accounting book, examples of standard forms and examples of their completion were given.

Separately, in the article, we also touched on the latest legislative innovations related to the maintenance of KUDIR in 2017. They talked about the prepared new form of the accounting book.

When keeping records, it is better to adhere to the above recommendations and then there will be fewer questions from the tax office and paperwork. It’s not difficult to fill out a couple’s book on your own; you can also use specialized online accounting services.

Surely many entrepreneurs will be interested in such a topic as KUDiR for individual entrepreneurs on the simplified tax system, a sample filling. We will consider the intricacies of maintaining this book, in addition, we will talk about how it is filled out on simplified taxation (USN).

Filling out the book of income and expenses

At the beginning of 2013, a law was passed that exempts individual entrepreneurs from the obligation to go through the process of registering the Book of Accounts with the tax authority. Recall that earlier it was necessary to certify the KUDiR at the Federal Tax Service Inspectorate without fail before you start filling it out. As soon as the tax period comes to an end (before April 30 of the next year), it is also necessary to take it to the tax authority so that the tax inspectorate employees put their signature and stamp on it confirming the acceptance of the document.At the moment, the availability of this book will not be checked with you. However, this is all temporary. As soon as a check comes to you, still go through to provide KUDiR. And if you don’t have it, you will be fined 200 rubles. It is allowed to fill in the book of accounting for income and expenses in electronic form, as well as on special forms. As soon as the year comes to an end, the book needs to be printed, neatly hem and put down page numbers. It must be stored for 4 years.

KUDiR for individual entrepreneurs on the simplified tax system involves the entry by the entrepreneur of all expenses and income, which are confirmed by the relevant documents. In most cases, this is a simple bank statement (bank payment orders, checks (trade, cash), invoices.

The order of filling in the KUDiR does not imply the presence of errors, although typos are quite common. This is a common thing that does not bode well. If you made a lot of mistakes, then you can correct them, a lot of effort is not required for this. If, KUDiR for IP on the simplified tax system is filled out electronically, then you can simply delete the incorrect data, after which you can enter the correct information into the form.

If the KUDiR filling pattern has a paper look, then the inaccuracies can be crossed out and the desired value written. However, each amendment must be confirmed by the signature of the individual entrepreneur, as well as his seal (if any).

What threatens an entrepreneur if incorrect data is indicated in the KUDiR?

Suppose the IP did not correctly calculate the tax, respectively, the procedure for filling out the KUDiR will contain incorrect information, in which case the IP will have to pay 20% of the total tax as a penalty. And if he deliberately hid the correct data, as a result of which the amount of taxes payable turned out to be less, then he faces a penalty in the amount of 40% of the tax.If tax payments are paid on time, then liability for incorrect information in the KUDiR can be avoided. These payments must be calculated correctly. Suppose you enter incorrect information on income in KUDiR, but pay the tax in full, then you will not be penalized. It is convenient to conduct KUDIR online in this online service.

A sample of filling out a book of accounting for income and expenses

The book of accounting for expenses and income consists of several subsections.Title page.

The first column "Taxpayer (full name of individual entrepreneur)" must indicate your initials.

The line “For 20 __ year” indicates the year when this book began to be kept.

We skip the “Enterprise Taxpayer ID” section, because we are an individual entrepreneur, not an enterprise. We need a line that is a little lower. It has the following name: "TIN of the taxpayer TIN (IP)". This is where you should write down your TIN.

The line object of taxation serves to indicate the taxation system for the work of an individual entrepreneur.

Please enter your address below.

Write down your current accounts below.

Now the title is filled, you can proceed to the first section.

The first section has 4 tables. Each of them reflects the activity for the 1st quarter.

1. Column No. 1 reflects the number of the operation.

2. Column No. 2 - Number and date of the primary document. Here the number of the supporting document and the date of the operation are prescribed.

3. Column No. 3 - the name of the organization, you can also indicate the number of the account from which expenses and incomes were transferred to you. It also briefly describes the entire process of the operation.

4. Column number 4 - fix all income, which are the basis of the entire tax base.

5. Column number 5 - serves to reflect all expenses.

Remember that column No. 5 is filled in only by those individual entrepreneurs who work on the simplified tax system.

If, in detail, consider the KUDiR for IP on the simplified tax system, a sample of filling, then this mandatory procedure will not be difficult to write.

One of the elements of control over the income of an entrepreneur is a book in which both his income and expenses are entered (KUDiR). Its maintenance is mandatory not only for preferential tax regimes, but also in some cases and with.

All about KUDiR on OSNO

With OSNO, the accounting book is required to be kept only by. Companies, incl. from this stage of control in this case are released. In it, entrepreneurs are required to display income received and expenses incurred. Moreover, it is worth remembering that an individual entrepreneur must fill out KUDiR if he applies:

And each option has its own characteristics. Therefore, being on the main system, the entrepreneur must apply the appropriate form of KUDiR. Its features:

- Accounting for the movement of funds is carried out on a cash basis.

- If an individual entrepreneur has several types of activities, then they are recorded in one book, but separately.

- It should also reflect the attitude of the entrepreneur to.

The book can be completed:

- In paper form.

- In an electronic version, but with the condition of its printing at the end of the reporting period (year).

The deadline for reporting on KUDiR to the Federal Tax Service is April 30th. That is, before this date, the accounting book for the past code must be certified by the inspector.

The video below will tell about the role of KUDiR for LLCs and individual entrepreneurs:

Filling out the book of income and expenses

If the book of accounts is kept in paper form, then it must be purchased. This responsibility lies with the entrepreneur. And when filling it out, you must follow these rules:

- All receipts and expenditures must be reflected in chronological order and be supported by primary documents.

- The main task is to ensure full and continuous accounting of indicators intended for calculating the base and amount of tax.

- The pages of the book should be numbered and laced. On the last page, this number must be confirmed by the signature of the entrepreneur and, if possible, a seal.

- If the records are kept in electronic form, then at the end of the KUDiR period, you must print and follow the same procedures as described above.

- Correction of errors is allowed only with the signature of the entrepreneur and the date. Correct carefully. Cross out with one line.

- The ledger and accounting are kept in parallel, and one does not exclude the other.

- At the beginning of each reporting period, a new book is opened. Its shelf life at the enterprise is 4 years.

Registration procedure

The book consists of the following parts:

- Title.

- 1st section (income with expenses).

- 2nd section with the calculation of the entrepreneur's expenses for fixed assets.

- 3rd section with the amounts of losses.

- 4th section with expenses that reduce the amount of tax (but this is only for).

The title page is issued immediately after the purchase:

- The accounting year and date of registration of the book are indicated.

- Entrepreneur's full initials and form.

- Below is the TIN.

- Then the object of taxation is recorded: income or income minus expenses.

- Next is the currency and its code.

- Full address.

- Bank and.

Section 1 is completed quarterly, with the results:

- For the quarter.

- For half a year.

- For 9 months.

- Per year.

Data is entered into a table of 5 columns:

- 1st - record number in order.

- 2nd - for entering the primary document (number, date) for which the funds were received (spent): through the cash desk, through the current account, by, as a return.

- 3rd - description (content) of the operation or action entered into the book.

- 4th - to record the income received as a result of this.

- 5th - fixes the expenses incurred in this case, including: material, wages, depreciation, and others.

- The 4th and 5th columns are filled in only if there are incomes (expenses) from the operation entered in the book.

Advances received are included in the income column of the period (quarter) when they are received, that is, by the date the money is credited to the account, and not by the date the entrepreneur fulfills his already paid obligations. This is more consistent with the cash accounting method in KUDiR.

The remaining sections of the KUDiR are not filled out by entrepreneurs on OSNO.

Filling out the book of accounting for income and expenses in 1C is described in this video:

Zero KUDiR

If during the reporting period the entrepreneur on OSNO did not have any movement either on accounts or through the cash desk, then, along with other types of reports, a zero ledger is also provided to the Federal Tax Service. That is, KUDiR is externally designed as a regular one, but with zeros in all columns where the actual display of the movement of funds is required.

Filling program

If the accounting book is kept in electronic form, then it is convenient to use software to fill it out. It could be:

- 1c accounting.

- Or another program for automatic accounting.

They can be purchased and installed through specialized companies. The price for them is quite high, but their use will allow you to accurately take into account in automatic or manual mode:

- Arrival of goods.

- Reflection of income by suppliers.

- Income and expenses for KUDiR.

Example

Sample filling KUDiR on OSNO